A New Fund for a More Rational Vintage

Every venture fund has a natural rhythm. Capital is raised, deployed into a portfolio, reserved for follow-ons, and, as the fund moves through its deployment cycle, a new vehicle becomes the logical next step. This is the process answer to why a fund raises again.

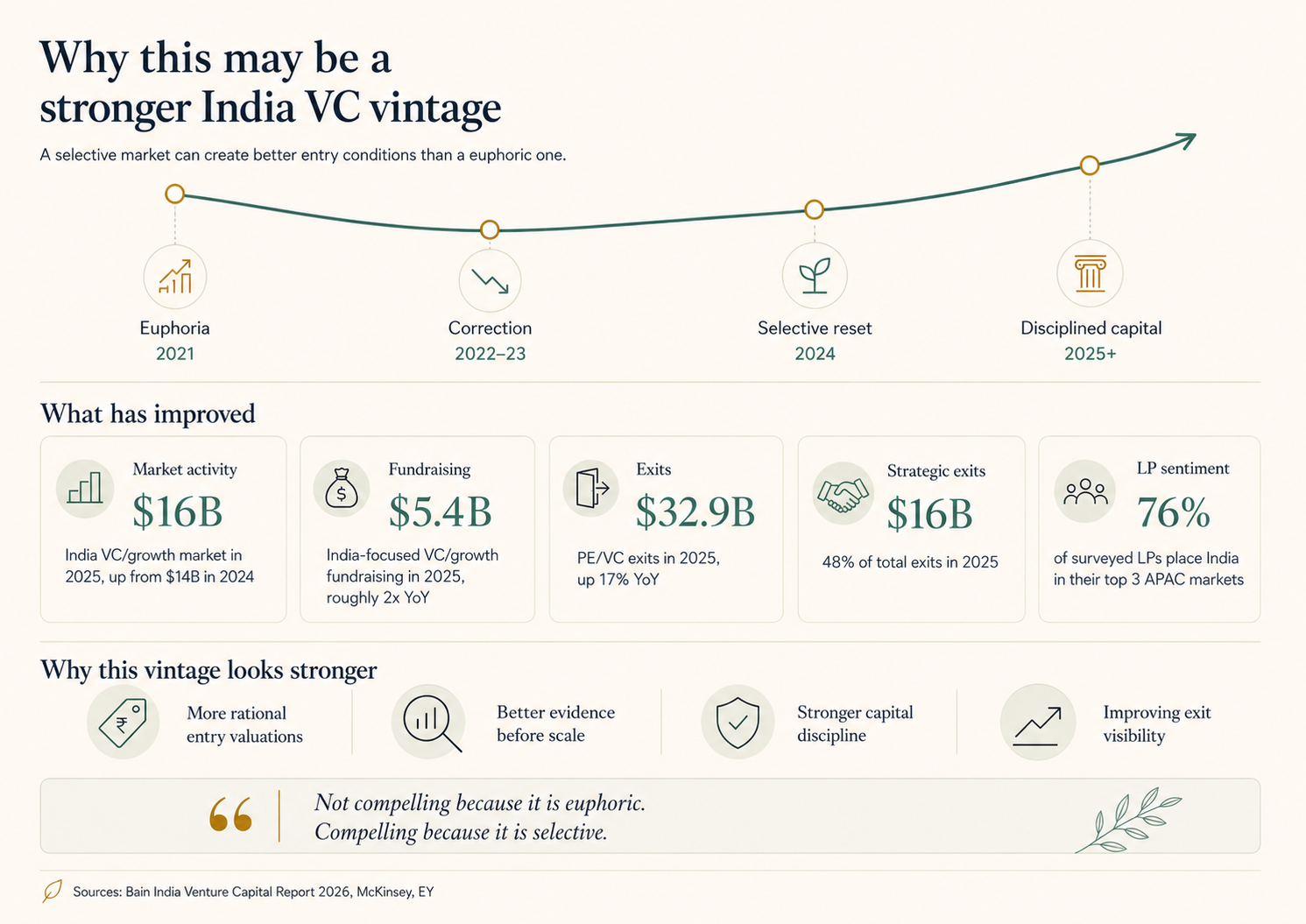

The more important question, however, is why this vintage deserves conviction.

Venture capital is highly sensitive to the conditions under which capital enters companies. Entry valuations, founder behaviour, availability of follow-on capital, exit visibility and the quality of competition all shape outcomes long before a company reaches maturity. On that basis, the current India venture environment is not compelling because it is euphoric. It is compelling because it has become more selective.

Bain’s India Venture Capital Report 2026 captures this well. India’s VC/growth market reached approximately $16 billion in 2025, up from $14 billion in 2024, even as broader private capital deployment softened. Unlike 2024, when the rebound was largely volume-led, 2025 saw a more balanced recovery across both deal volumes and average deal size. Larger $100 million-plus rounds returned, $250 million-plus deals doubled year on year, and small and mid-stage activity held firm.

This matters because it shows that capital is not simply returning everywhere. It is returning with greater discrimination. The market is still forming new companies, but it is also demanding better evidence before companies scale.

That formation signal is visible at the early and mid stages. Series A to C deal volumes maintained momentum in 2025 and rebounded to 2022 levels, while seed volumes increased modestly, supported by investor focus on new waves of innovation across consumer tech, software/SaaS, deeptech and AI/generative AI. For an early-stage fund, this is the relevant zone: before consensus has fully formed, but after the market has corrected some of the excess behaviour of the previous cycle.

The sector mix also points to a more durable opportunity set. The earlier India venture cycle was largely about digitising access. The next cycle increasingly appears to be about digitising capability. Software/SaaS funding rose approximately 1.5 times year on year, with AI-led product evolution and global expansion bringing mature companies back to market. AI and generative AI-native B2B companies gained traction in vertical use cases, particularly in BFSI and healthcare, where applications are moving beyond pilots into production-scale automation. Fintech deal value rebounded 2.2 times, with investor interest shifting towards RBI-aligned models and wealth-focused platforms. Even consumer tech has become more measured, with capital moving towards verticalised platforms, tighter supply chains, retention-led growth and disciplined unit economics.

The capital market around these opportunities is also maturing. India-focused VC/growth fundraising roughly doubled in 2025 to approximately $5.4 billion, driven by larger $100 million-plus vehicles. Importantly, this was not indiscriminate fund formation. Capital was led by established managers, while first-time managers found it harder to raise as LPs leaned towards proven teams amid improving exit visibility.

This aligns with the global LP view. McKinsey’s survey found India to be the most attractive private-market destination in Asia-Pacific, with 31% of surveyed LPs ranking it first and 76% placing it in their top three. More than 50% of surveyed LPs expect to increase allocations to India-dedicated funds, while only 5% expect a reduction. In other words, India is moving from being an emerging-market allocation to a more intentional part of global private-market portfolios.

The exit picture is also improving. EY reports that Indian PE/VC exits reached $32.9 billion in 2025, the second-highest level recorded, up 17% over 2024. Strategic exits grew 211% year on year to about $16 billion, accounting for 48% of total exits. This does not mean India’s exit challenge has disappeared, but it does suggest that public-market, strategic and structured liquidity pathways are becoming more credible.

There are still near-term risks. 2026 began with muted deployment, with January investments 37% lower than December 2025 and 36% lower than January 2025. Geopolitical volatility, currency pressure, valuation gaps and public-market volatility remain real constraints.

But that caution is part of the opportunity. A hot market can reward speed over judgement. A selective market rewards discipline. For a new fund, this is a stronger entry environment: founders are more grounded, capital is more discerning, sectors are becoming more infrastructure-led, LP appetite for India is rising, and exits are becoming more visible.

The natural reason to raise a new fund is deployment. The more strategic reason is vintage quality. On that measure, this moment is well placed.